From the Senator's Desk . . .

October 19, 2007

As you may know, our state and nation are experiencing a dramatic increase in foreclosures in the subprime mortgage market as countless families find themselves unable to meet their financial commitments. This month, I requested that Governor Perry call a special session in 2008 to address this crisis.

Written by Senator Eliot Shapleigh, www.shapleigh.org

"Protecting Texas Families - The Subprime Foreclosure Crisis in Texas"

As you may know, our state and nation are experiencing a dramatic increase in foreclosures in the subprime mortgage market as countless families find themselves unable to meet their financial commitments. Since 2003, I have written Governor Rick Perry, Lt. Governor David Dewhurst, and even former Chairman of the Federal Reserve Alan Greenspan on this important issue. This month, given the high volume of subprime lending in Texas over the past few years, I have requested that Governor Perry call a special session in 2008 to address this crisis.

Nouriel Roubini, a professor at New York University and head of Roubini Global Economics, predicts a resulting recession in the near future. He contends that if the economy slips into recession, "then you have a systemic banking crisis like we haven't had since the 1930s. The cost could be as high as $1 trillion."

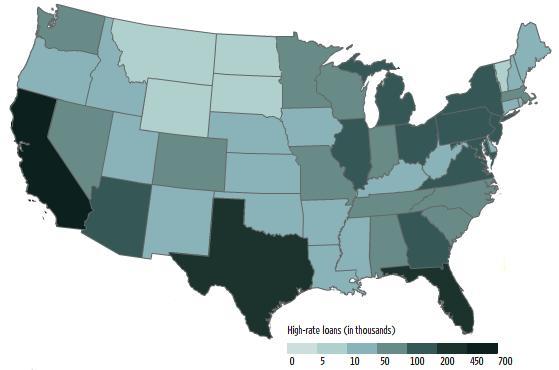

This spike in foreclosures has been associated with declines in stock markets worldwide, coordinated national bank interventions, and bankruptcy of several mortgage lenders. Below, you will find a national map showing the number of high rate loans issued in 2006, the driving force behind the current foreclosure crisis.

Number of High Rate Loans Issued in 2006

Click here to view larger image.

Source: Rick Brooks and Constance Mitchell Ford, "The United States of Subprime," The Wall Street Journal, October 11, 2007.

I am extremely concerned about the fiscal impact on Texas, particularly on the budget in the 81st Legislative Session. For that reason, I am urging Governor Perry to act now and protect Texas families from what may well be a Texas tsunami of mortgage foreclosures.

Specifically, I have asked that Governor Perry call a special session in early 2008 so that together with the Legislature, he can help us act to protect our state's homeowners, communities, and school districts. I have asked that he frame the call around the following concepts:

- Working with mortgage lenders and servicers to maximize alternatives to foreclosure so that more homeowners can keep their homes. Inevitably, some discretion for mortgage lenders and servicers is built into the decision of whether to foreclosure, and lenders and servicers must maximize this discretion to allow homeowners to seek out all potential means of avoiding foreclosure and the loss of their home;

- Providing increased funding for non-profit housing counselors and the expansion of educational efforts to make borrowers aware of options to work out delinquencies, with funds distributed based on areas of greatest need. Counseling and other educational services will help prevent foreclosure, in addition to building budgeting skills and connecting Texans with community resources; and

- Requiring counseling before closing on certain subprime and high risk mortgage loans. Texas must empower future homeowners with tools and knowledge to make the most informed decision regarding their home loan.

If Governor Perry chooses not to act now, any legislative change will be delayed until the next regular session in January 2009. In that case, I have asked that he convene a Governor's work group to develop a statewide response to the foreclosure crisis and subsequent legislative recommendations.

Ohio, which has one of the highest foreclosure rates in the country, recently released the final report from the Ohio Foreclosure Prevention Task Force. Created in March 2007 by Governor Ted Strickland, the Task Force's mission was to provide a unified response to improve prevention methods and manage foreclosure issues in Ohio. The Task Force's report was issued on September 10, and its recommendations will help the state focus on the escalating crisis.

If Texas' leaders do not act, I fear that our state could be faced with a deficit similar to or worse than that in 2003. In our state today, there are concerns that the new margins tax will not bring in sufficient revenue. Those fears are now compounded with the new threat that exists due to the exceedingly high number of foreclosures. Foreclosures impact many aspects of the economy, and our state's leaders need to take a hard look at these numbers. The current glut of foreclosures we are experiencing could cause Texas' property values to dive due to significant foreclosures. Obviously, if property values drop, school tax revenues drop, creating a demand for increased state revenue. Houston’s experience in 1986 demonstrates how foreclosures and real estate values can dramatically affect property values and school tax revenues. This will have a significant impact on the state's bottom line when we return to Austin for the 81st Legislative Session.

As you may know, Texas has some of the highest loan rates in the country. According to the Corporation for Enterprise Development, Texas ranked number 43 in the country in the percent of all mortgage loans that are subprime loans. Of the ten highest subprime MSAs in the U.S., Texas is home to seven:

MSA Ranking by Overall Percentage of Subprime Refinance Loans

|

Rank |

MSA Name |

Population |

Conventional Refinance Loans |

Percent Subprime |

|

1 |

El Paso, TX |

679,622 |

1,767 |

47.82 |

|

2 |

Corpus Christi, TX |

380,783 |

1,061 |

46.84 |

|

3 |

Laredo, TX |

193,117 |

342 |

45.32 |

|

4 |

Killeen-Temple, TX |

312,952 |

683 |

44.80 |

|

5 |

Beaumont-Port Arthur, TX |

385,090 |

1,160 |

44.48 |

|

6 |

Miami, FL |

2,253,362 |

10,701 |

42.67 |

|

7 |

Columbus, GA-AL |

274,624 |

1,799 |

42.63 |

|

8 |

San Antonio, TX |

1,592,383 |

5,270 |

41.90 |

|

9 |

Memphis, TN-AR-MS |

1,135,614 |

7,577 |

41.86 |

|

10 |

Galveston-Texas City, TX |

250,158 |

944 |

41.63 |

Source: Texas Low Income Housing Information Services, using data from the May 2002 Risk or Race? Racial Disparities and the Subprime Refinance Market report by the Center for Community Change.

The high number of subprime mortgage loans has finally caught up with Texas and, indeed, the entire country. In the McAllen metropolitan area, over 39 percent of the mortgage volume between 2004 and 2006 were high rate loans. The inevitable result of these numbers are higher foreclosures. In August 2007, Texas reported 16,970 foreclosure filings, the fourth highest total in the nation for the month. These figures represent a 36 percent increase over July 2007, and the state's foreclosure rate of one foreclosure filing for every 532 households was 9th highest among the states. On the following page, please find a chart of July 2007 foreclosures in Texas' five largest counties.

Texas Foreclosure Activity - August 2007

| County | August 2007 Foreclosures | 1 in every # households |

| Harris | 3,176 | 459 |

| Dallas | 3,205 | 285 |

| Tarrant | 2,522 | 253 |

| Bexar | 1,318 | 435 |

| Travis | 678 | 577 |

Source: RealtyTrac U.S. Foreclosure Market Report

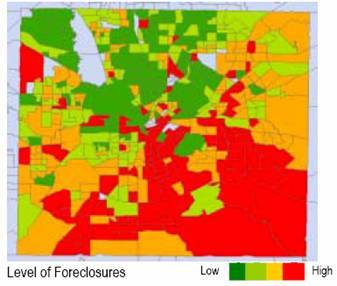

Here is what the 2005 to 2006 foreclosure activity looked like in Dallas County, the county with the highest number of foreclosures in August 2007:

Source: Texas Department of Housing and Community Affairs

Nationally, the numbers are alarming as well. In the most recent quarterly report issued by the Mortgage Bankers Association, this quarter’s foreclosure starts rate is the highest in the 53-year history of the survey, with the previous high being last quarter’s rate. According to RealtyTrac, foreclosure filings across the U.S. nearly doubled last month compared with September 2006, jumping from 112,210 to 223,538.

The high rate mortgages that are causing the incredible jump in foreclosure rates are not just limited to minority, low-income borrowers. Indeed, a recent analysis by The Wall Street Journal shows that, in addition to low-income areas, high rate lending rose sharply in middle-class and wealthy communities. The problem is not over, either. As much as $600 billion in adjustable-rate subprime loans are due to adjust to higher rates by the end of 2008, thus putting more and more borrowers in precarious financial situations.

As your Senator, I am working to address this issue and take immediate steps to help Texas prepare for and respond to the ongoing foreclosure crisis. For more information, please visit my website at www.shapleigh.org/reporting_to_you.

Texas is worth the fight—keep the faith!

Eliot Shapleigh

![]()

![]()

Related Stories