Tax Equity Note Confirms that Most Texas Families Would Pay More Under HB 3, the “Tax Relief Bill”

March 8, 2005

The Legislative Budget Board has calculated that the changes proposed by HB 3 by Rep. Keffer would increase taxes paid by 80% of Texas families.

Written by Dick Lavine, Center for Public Policy Priorities

WHAT HB 3 WOULD DO

HB 3 by Rep. Keffer is intended to raise certain state taxes in order to reduce school property taxes. It is explicitly designed to be revenue neutral – any new state revenue raised by the bill is intended solely to cut property taxes. This is the chief problem with the bill.

More than cutting property taxes, Texas needs to improve public education, adequately fund health and human services, increase access to higher education, and support other important public services. HB 3 is flawed in its basic purpose.

The largest single source of revenue in HB 3 is an increase in the state sales tax rate by a full penny – from the current 6.25% to 7.25%. This would be the highest state sales tax rate in the nation. No other state imposes a sales tax greater than 7.0%.

More than one-half of the revenue in HB 3 would come from the increase in the sales tax rate, a similar increase in the motor-vehicle sales tax rate to 7.35%, and an expansion of the sales tax base to include car repair, bottled water, and other items.

The payroll tax would assess the full tax rate of 1.15% only on workers earning less than $90,000 per year, and would completely exclude many highly paid professionals. This tax would account for only about 30% of new revenue.

The $1.00 increase in the cigarette tax would generate roughly 12% of the new revenue in the bill.

MOST FAMILIES WOULD PAY MORE

The tax equity note for HB 3, prepared by the Legislative Budget Board (LBB), calculates the “final incidence” for the proposed tax changes. Incidence takes into account that the effect of tax changes is shifted over time from the initial impact on business to a final impact on families in prices, wages, or profits. It also calculates the cost to families at different income levels of the increased sales and tobacco taxes, as well as lower property taxes.

The tax equity note concludes that 80% of Texas families would see an increase in total taxes as a result of HB 3. Only the 20% of families with an income over $100,000 would be expected to actually benefit from the bill.

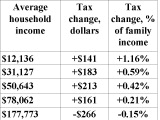

This chart shows CPPP’s calculations of the impact of HB 3, based on the LBB’s tax equity note. The equity note divides all households into ten equal groups; this Policy Page pairs these groups into five equal income categories to make it easy to view. Each income group contains one-fifth (20%) of all Texas households – 1.65 million households.

The first column shows the average income of families in each income group, the second column shows the tax change due to HB 3 expressed in dollars, and the third column shows the tax change in terms of the percentage of family income that would be lost or gained because of the bill. Note that only families in the highest income group would see a decrease in their tax burden.

Average household income

Tax change, dollars Tax change, % of family income. An additional calculation shows that families in the top one-tenth by income, with an average income of $240,000, would see a tax cut of $487 a year, equal to 0.20% of their family income.

TEXAS' TAX SYSTEM

Texas has a very unfair tax system – the families with the lowest income pay the highest percentage of their income in taxes; the families with the highest income pay the lowest percentage of their income in taxes. In other words, those who can least afford it pay the most. A system that takes a higher percentage of the income of a lower-income family is called “regressive.” Texas has the fifth most regressive state and local tax system of the 50 states.

HB 3 would appreciably increase the regressivity of Texas’ tax system by increasing the tax load on lower- and middle-income families, while decreasing the taxes paid by upper-income families.

The underlying cause of this tax shift is primarily the use of the regressive sales tax to replace the less regressive property tax. For more details on tax incidence, see Who Pays Texas Taxes?

FEDERAL DEDUCTIBILITY

The tax equity note points out that HB 3 would result in an initial increase in revenue of $213.9 million, but would ultimately increase the taxes of all households by $709.3 million.

This discrepancy is largely due to the replacement of property taxes, which are deductible from federal personal income taxes, by sales taxes, which are generally not deductible. A temporary provision allows sales taxes to be deducted in 2004 and 2005, but this deduction will expire before the time period covered by the tax equity note.

For more information on the sales tax deduction, see Temporary Sales Tax Deduction No Excuse for Raising Sales-Tax Rate,

A BETTER CHOICE

To learn what CPPP recommends to lower property taxes while adequately funding our state, see The Best Choice for a Prosperous Texas

![]()

![]()

Related Stories

![]()

Fair Use Notice

This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a "fair use" of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. For more information go to: http://www.law.cornell.edu/uscode/17/107.shtml. If you wish to use copyrighted material from this site for purposes of your own that go beyond "fair use", you must obtain permission from the copyright owner.